Market Recap

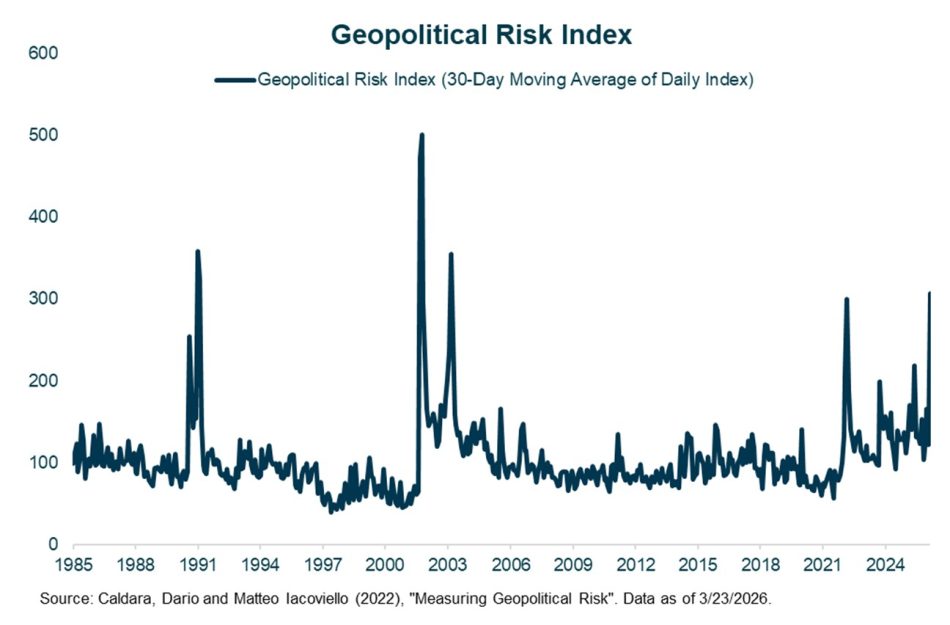

Investors were barraged with a staggering number of events during the quarter. There was no shortage of geopolitical headlines with the year kicking off with the capture and extradition of Venezuela’s then-president, Nicolás Maduro. And as the first quarter ends, conflict in the Middle East dominates the market narrative and is roiling energy markets.

In the first quarter, the S&P 500 fell 4.3%. U.S. equities were marginally positive on the year until the conflict with Iran commenced in late February. The bar chart below shows how different asset classes have performed since the onset of the war at the end of February. Foreign equity markets have suffered worse than domestic markets. A stronger U.S. dollar in March contributed to some of the underperformance—another possible explanation is that higher energy prices have more of a negative impact on countries that import much of their energy. The U.S. has become a net exporter of oil in recent years and much less reliant on the Middle East for energy. Other nations, particularly many in Asia, import much of their energy through the Persian Gulf.

Unsurprisingly, energy stocks (up 38.2%) were the top performer within the S&P 500 during the first quarter. More defensive sectors, such as utilities, also outperformed. Mega-cap tech stocks were the laggards during the first two months of 2026 as fears around elevated AI spend and a growing concern that many software stocks could see their moats weakened by AI agents. The S&P North American Expanded Technology Software Index has already fallen more than 24% this year and is now down in-excess of 30% from its high last September.

After delivering another rate cut last December, the Fed held rates steady at their two meetings in 2026. The Fed funds rate remains at 3.5%-3.75%. Since the onset of the war, the market has priced out any additional rate cuts this year. The implied number of cuts for 2026 was about two cuts at the end of February—however, the market is now pricing a Fed that will hold rates at current levels. At one point in March, the market started pricing in Fed rate hikes in 2026, however, I believe this was an overreaction and that central banks around the world are unlikely to hike rates this year (more on that below). U.S. rates have moved higher on fears of higher inflation stemming the spike in energy prices. After closing below 4% at the end of February, the 10-year Treasury rate has jumped to nearly 4.4% in recent days. The two-year Treasury, which is often cited as a good proxy for the Fed funds rate, has increased nearly 50 basis points to 3.9%.

Investment Outlook and Portfolio Positioning

Despite all the events of the quarter, the S&P 500 is only 6% off the all-time high it reached in January. Broadly, the global economy is still expanding, and inflation continues to moderate despite all the negative headlines. S&P 500 earnings growth grew at a 14% clip last year and is expected to grow 13.2% year-over-year in the first quarter, according to data from FactSet. For now, corporate profits and the broader economy continue to show resiliency despite all the gloom.

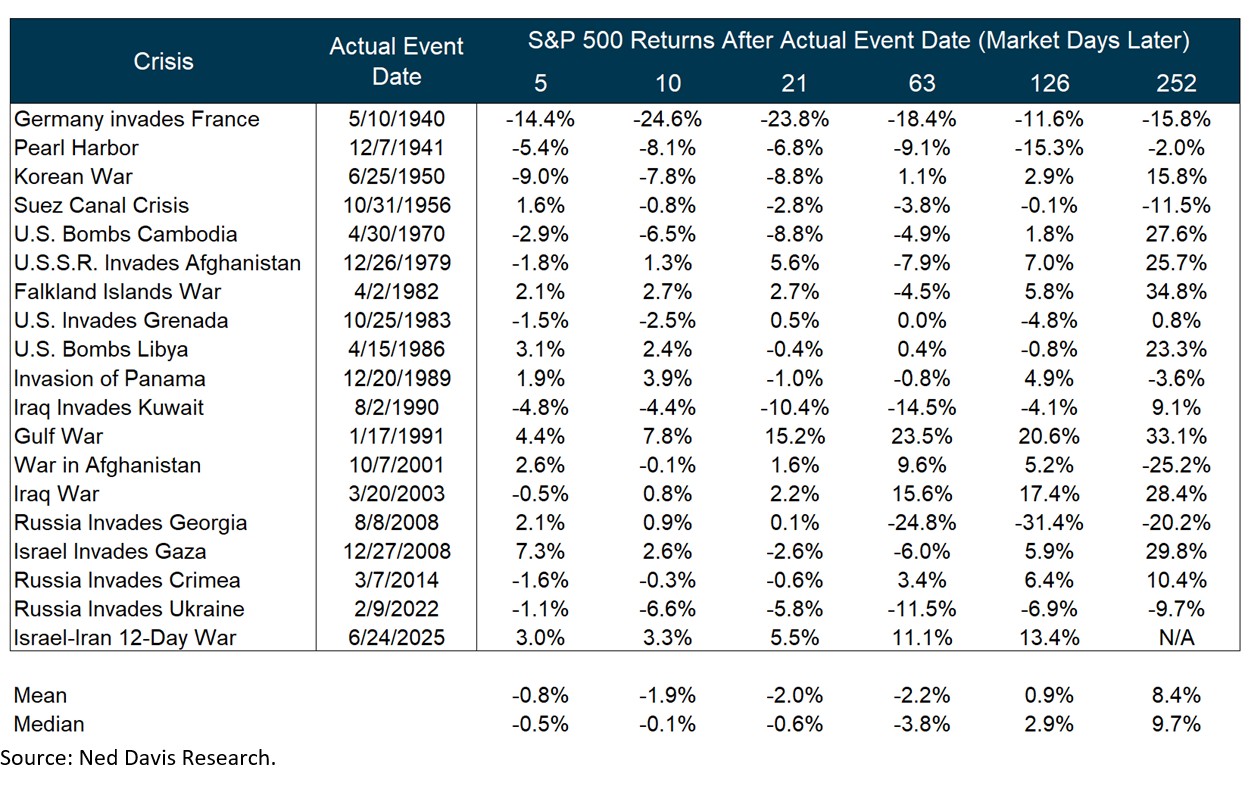

While geopolitical shocks can trigger sharp drawdowns, history suggests the impact is typically short-lived. Markets tend to re-price uncertainty quickly, with most of the reaction happening over days and weeks rather than quarters or years. Unless the event materially changes the path of the economy, inflation, or policy, risk assets can remain supported. The table below from Ned Davis Research shows the market reaction to military events since World War II. The current conflict in Middle East has certainly resulted in negative equity returns, but nothing outside of the historical norm.

The conflict’s duration will largely determine the impact on the global economy. With the Strait of Hormuz effectively shut, 20 million barrels of oil that transit the Strait daily are stranded. This accounts for roughly 20% of daily global oil demand. Liquified natural gas (LNG) is also heavily impacted by events in the Middle East. Qatar is responsible for 20% of global LNG supply and at the moment 100% of this is offline due to the war. It has been reported that Iran targeted and damaged a portion of Qatar’s Ras Laffan LNG complex, resulting in roughly 17% of their capacity to be taken out and that it could be years to repair and bring back production to normal levels. Any escalation that results in additional energy infrastructure being damaged will have lasting effects on the energy market.

Oil and gas fields are not like faucets—they cannot just be turned off and on. Once they are shut in, there are engineering and geological risks that don’t guarantee their resumption at previous production levels. Restarting these fields will take weeks to months, plus another 3-4 weeks for tankers to transit through the Persian Gulf and to Asia. The longer the Strait of Hormuz remains closed, the worse it will be for the global economy. Recent signs of de-escalation from President Trump have given markets some hope. And it has been reported that Iran will allow ships from “non-hostile” countries (i.e., countries that aren’t supporting acts of aggression against Iran). However, daily tanker transits through the Strait of Hormuz remains essentially non-existent.

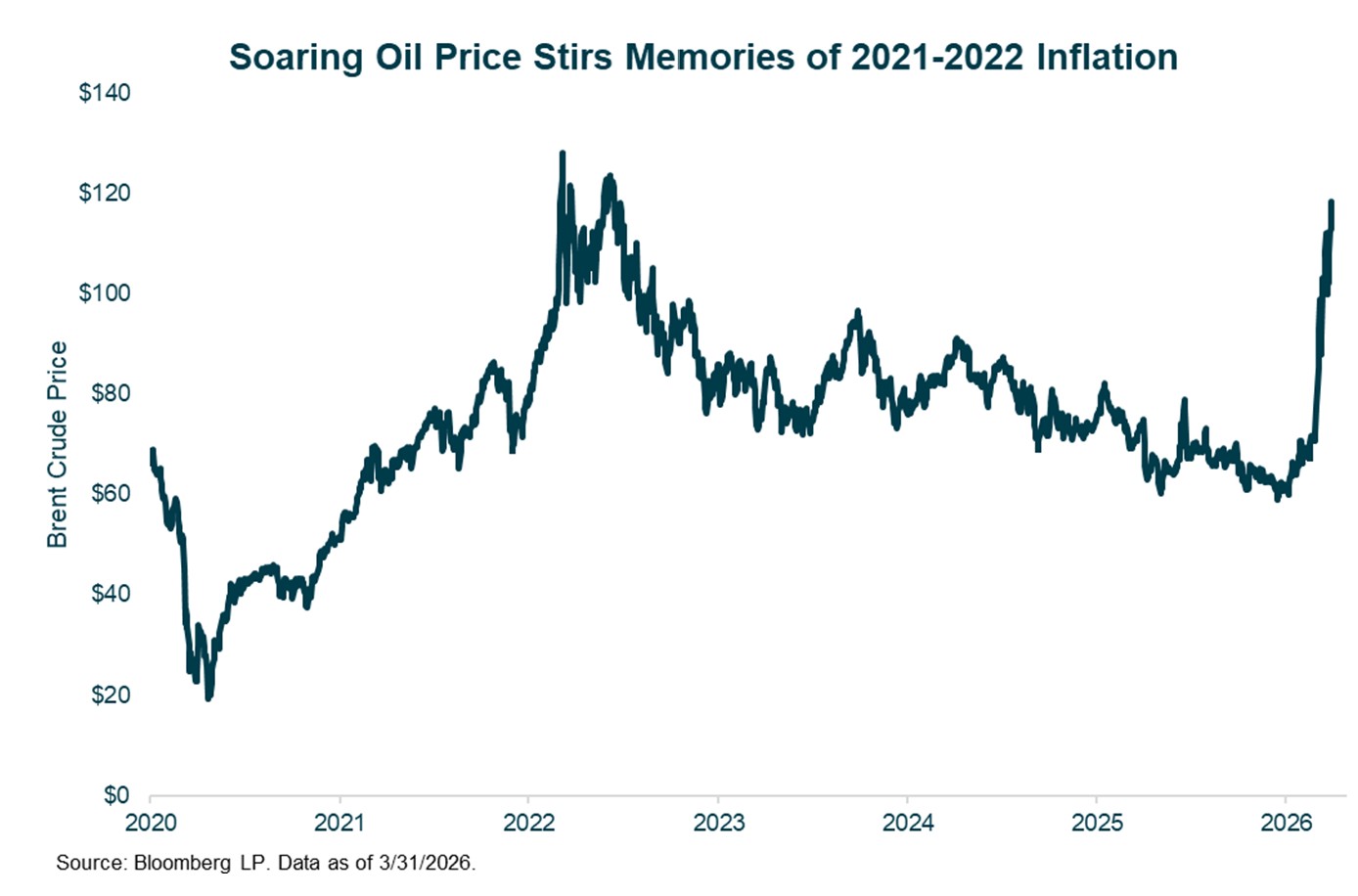

Understandably, the conflict in Iran has sent oil prices higher and is stirring memories of the inflationary spike of 2022 following the start of the Ukraine/Russia war. Broadly speaking, the current facts lead me to believe that today’s environment is different than from a few years ago. Back in 2022, inflation was driven by multiple forces that all came together at the same time—massive fiscal stimulus, ultra-accommodative monetary policy, a surge in money supply, pent-up demand from the pandemic, and disruptions to supply chains. Higher energy costs certainly played a role in the inflation spike; however, it was far from the only factor. Today, many of these factors are not in play. Rates are significantly higher, liquidity is being pulled from the system, the labor market has cooled down, and wage growth has decelerated. For the moment, any increase in inflation in the coming months or quarters will be driven by supply constraints rather than excess consumer demand.

Research from the Federal Reserve suggests that energy prices accounted for only a portion of the overall inflation increase. The Fed estimates that the oil price spike added roughly half a percentage point to overall inflation during 2022. Inflation has certainly cooled in recent years (see chart below), however, it remains above the Fed’s 2% target. Central Banks tend to focus on core inflation readings, i.e., those that exclude the more volatile food and energy prices. Given this, the Fed is more likely to respond to higher oil prices by holding rates where they are instead of hiking them. We are seeing this in the futures market where further rate cuts this year are being priced out of expectations. For now, my current base case is that the current oil shock is far more likely to produce a temporary bump in headline inflation rather than a repeat of the broad and persistent inflation cycle experienced a few years ago.

Closing Thoughts

The conflict in Iran has introduced a number of unknown variables into the investment outlook. Thus far, markets have largely looked through the clash; however, with each passing day the impact on the global economy becomes greater. Energy prices are rising quickly, with Asian and European economies having more exposure than the U.S. I do not believe central banks will react to an energy price spike, however if the conflict drags on and energy prices remain elevated it is likely that other aspects of inflation will increase, pushing on living standards and potentially forcing the central bank’s hand.

Absent the conflict in Iran, my outlook continues to remain constructive, with real GDP growth and supportive consumer spending and ongoing investment in infrastructure, energy and Artificial Intelligence all expected to enhance productivity.

Despite recent weakness, equity market fundamentals remain strong. We have begun to see market leadership broaden away from mega-capitalization technology stocks to smaller and more value orientated companies, providing crucial breadth for the market. Importantly, corporate earnings expectations continue to expand, with the S&P 500 earnings expected to grow 13.2% in 2026 according to FactSet (up from 12.8% at year-end).

Credit fundamentals continue to remain sound. The market has now discounted lower policy rates; however, it is my belief this will revert with more certainty surrounding the Iranian conflict. Attractive starting yields have resulted in fixed income returns increasingly driven by income rather than price appreciation.

There is no question the tail risks have increased as a result of the Iranian conflict, however with the range of outcomes so wide I do not believe it is prudent to make any large-scale changes as a one size solution does not fit all clients. I remain vigilant to the changing situation and thank you for your continued trust and partnership.

Jeff 04/11/26

Certain material in this work is proprietary to and copyrighted by iM Global Partner Fund Management, LLC and is used by Bogue Asset Management LLC with permission. Reproduction or distribution of this material is prohibited and all rights are reserved.