Market Recap

Global equity markets continued their ascent in the third quarter, driven by strong corporate earnings growth and expectations of easing monetary policy. Despite investor concerns related to a slowing economy, tariffs, and a looming government shutdown, the S&P 500 gained 8.1% over the quarter, ending near an all-time high, lifting its year-to-date return to over 14.8%. The tech-heavy Nasdaq posted a 11.4% return, lifted by continued optimism around AI-driven productivity and capital investment in cloud infrastructure. Large-cap growth stocks (Russell 1000 Growth) were up 10.5% nearly doubling value stocks’ (Russell 1000 Value) 5.3% gain. Small-cap stocks (Russell 2000) had a strong quarter (up 12.4%), outperforming large-cap stocks amid hopes that lower interest rates would benefit the asset class.

Internationally, developed market stocks (MSCI EAFE) gained 4.8% in the quarter, lifting their year-to-date return to over 25%. Emerging markets (MSCI EM) rose 10.6% in the quarter and are now up more than 27.5% year to date. Gains in the quarter were driven largely by easing global financial conditions and attractive valuations. Year to date, developed international and emerging market stocks are still outperforming domestic stocks, thanks to a roughly 10% decline in the U.S. dollar.

In the U.S. fixed-income market, after holding rates steady for the first eight months of the year, the Federal Reserve resumed rate cuts in September. Against this backdrop, investment-grade core bonds finished the quarter up 2.0% (Bloomberg US Aggregate Bond), while high-yield bonds were up 2.4% (ICE BofA US High Yield).

Investment Outlook and Portfolio Positioning

Markets are always reacting to news, but today it feels even more pronounced. Every data release, policy comment, or geopolitical headline seems to carry an outsized influence on investor sentiment. This heightened sensitivity seems justified, as investors try to determine the path forward.

Against this noisy backdrop, there are reasons for optimism. One important tailwind comes from monetary policy. The Federal Reserve’s recent rate cut, after a prolonged pause, provides a constructive backdrop for both equities and bonds. Lower rates reduce borrowing costs for consumers and corporations, potentially fueling further investment and spending. History also offers perspective. A study by J.P. Morgan found that when the Fed cuts rates with the S&P 500 within 1% of an all-time high, the index has averaged a 15% gain over the following 12 months.

The consumer also remains a source of strength. The U.S. economy is primarily driven by consumption, often described as the backbone of growth. Spending has held up well across much of the economy, even after adjusting for inflation. While income and spending levels are not distributed equally, i.e., there are meaningful disparities across households, overall consumption has been supported by real wage growth that has outpaced inflation in many segments. This has enabled households to absorb higher costs without meaningfully pulling back. Balance sheets, meanwhile, remain generally healthy, the result of higher brokerage accounts and stable housing values.

Corporate fundamentals add another layer of support. Earnings growth rose 11.7% in the second quarter, making it the third consecutive quarter of double-digit growth. Many companies reported expanding margins, improved efficiency, and positive forward guidance. These results provide a foundation for higher equity valuations.

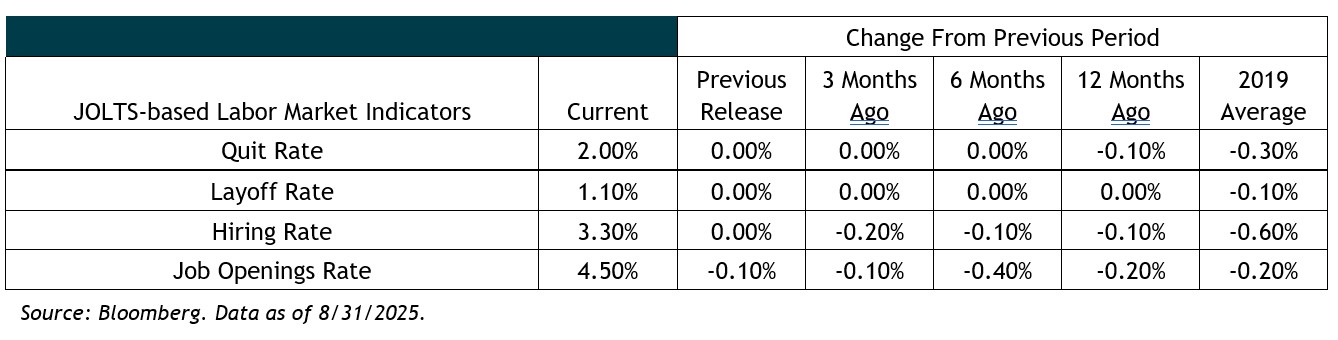

Of course, risks remain. I am closely monitoring the labor market. Key indicators such as quit rates, layoff rates, and initial unemployment claims have all flatlined. We seem to be at stall speed, and conditions could shift either way, so I am monitoring developments closely, especially the unemployment rate.

Since April, job gains averaged around 53,000 per month, which aligns closely with estimates of breakeven job levels needed to keep unemployment steady. I am not yet seeing broad-based layoffs or the kind of deterioration that typically signals an outright downturn. In the table below, I show some current key labor market stats compared to prior periods.

Deciphering the job market data is not as easy as reading the headlines. In recent years, immigration has led to large swings in labor supply and distorted the relationship between payroll growth and unemployment. When labor supply expanded quickly in 2023 and 2024, job gains looked strong but were outpaced by labor force growth, leading to higher unemployment. Conversely, when supply growth slowed in late 2024 and early 2025, job growth weakened but the unemployment rate held steady. More recently, employment growth has slowed further, yet the number of job seekers remains roughly in line with available jobs. The key point is that payroll growth can look strong when conditions are deteriorating and appear weak when the market is relatively balanced. Today’s combination of modest job growth and a stable unemployment rate suggest the labor market is slowing but not collapsing. I continue to watch the data closely for signs of further weakening.

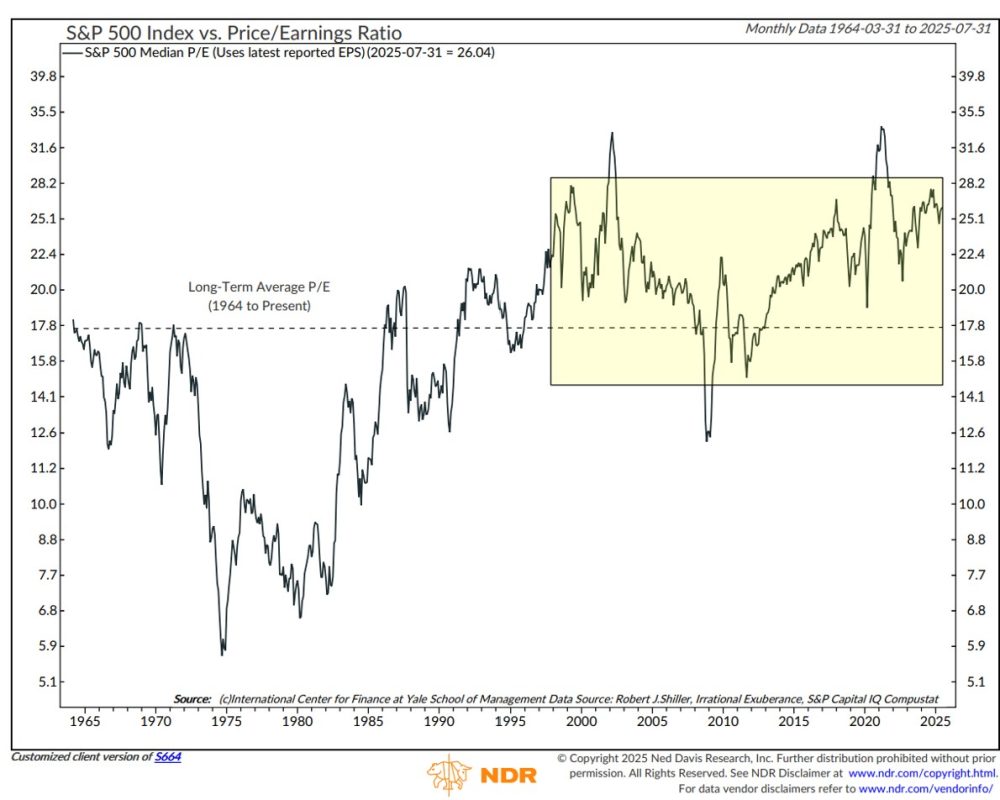

Within equity markets, at the beginning of the year, consensus return expectations for U.S. equities were in line with the historical average of about 8%. Year to date, U.S. stocks have exceeded those assumptions reaching new all-time highs in September. Naturally, current price levels raise the question of valuation – are stocks too expensive and should we take risk off the table? I don’t think so. Today, the S&P 500 trades at roughly 26x trailing 12-month earnings compared to a long-term average of 17.8x. These elevated levels are not lost on me, and they remain a critical factor I monitor closely. Yet context matters. As the chart below illustrates, the S&P 500 has traded above its long-term average for most of the past 25 years.

So, what is the “right” multiple? I believe the historical average of 17x is too low for today’s market. A higher fair-value multiple is warranted given structural changes in the U.S. economy and the composition of the U.S. equity market (S&P 500).

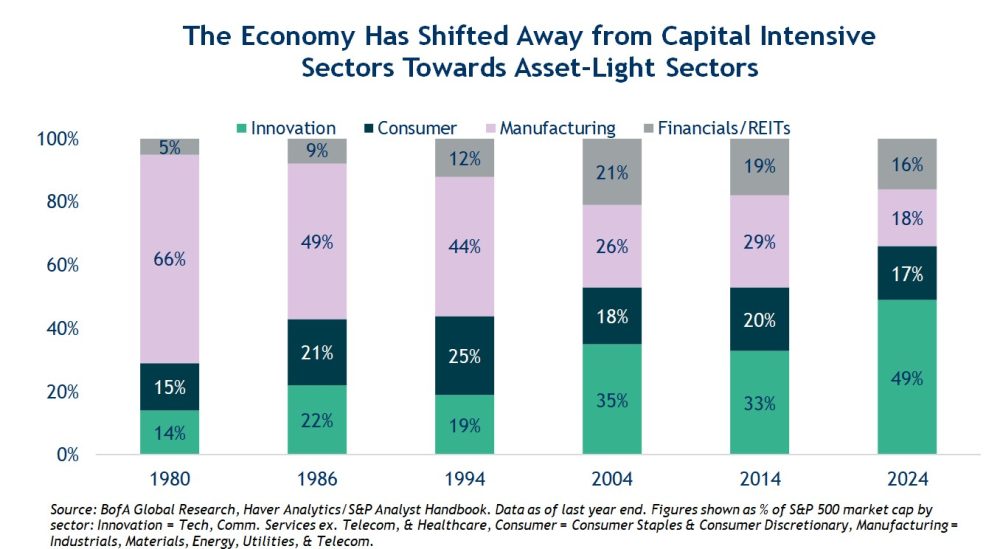

Today’s economy looks very different than past decades. Comparing today’s multiples to those of the 20th century without acknowledging this shift can be misleading. Back then, capital-intensive industries with lower margins and higher reinvestment needs dominated the market.

Now, as shown in the chart below, technology and service-oriented companies, which scale efficiently, require less capital, and earn higher margins, represent a much larger share of the U.S. equity market. In 1980, capital-intensive businesses made up two-thirds of the S&P 500 index, while asset-light firms were less than 15%. Today, roughly half of the index is represented by innovation-driven companies, while manufacturing has shrunk below 20%.

Of course, I am mindful that exuberance can push valuations beyond reason. Excessive risk-taking and investor optimism will always have the potential to drive markets to extremes. However, I believe there are sound, structural reasons why equilibrium multiples today are higher than in previous decades. In my view, a fair base-case multiple is likely in the low-20x range, with peaks in the upper-20s and troughs closer to the historical average of 17x. Today, valuations are at about 22x forward earnings, which is high relative to history, but not overly excessive.

Within bond markets, after holding rates steady for the first eight months of the year, the Federal Reserve resumed rate cuts in September. The Fed stated the cut was “risk management,” taking a more cautious stance toward slowing growth and softening labor conditions. Yet the path forward remains far from certain. While the Fed emphasizes data dependency and balancing the risks of inflation versus economic growth, markets are pricing in a more aggressive easing trajectory.

In my view, today’s environment suggests maintaining flexibility, emphasizing credit selectivity, and closely monitoring economic data that will shape market expectations. I continue to invest with higher-yielding, flexible bond funds run by experienced teams with broad opportunity sets. At the same time, I am maintaining meaningful exposure with core investment grade bond funds, given attractive starting yields and potential downside protection.

Closing Thoughts

We enter the final quarter of the year with both opportunity and uncertainty. Equities are supported by resilient earnings, healthy consumer demand, and a more accommodative Fed, yet valuations remain elevated, and policy debates loom large. In fixed income, tight spreads reflect strong corporate fundamentals even as fiscal pressures and policy divergence create risks at the long end of the curve. Labor markets are softening but not collapsing, reinforcing the view that growth is slowing rather than outright stalling.

This is a moment to stay disciplined. Near-term volatility and policy noise will likely continue, but fundamentals (i.e., healthy balance sheets, consumer spending, and improving breadth in equity markets) are providing a constructive backdrop. I continue to maintain diversified portfolios, balancing risk and opportunities, and positioning to benefit from long-term secular trends while staying alert to evolving macro and policy risks.

I thank you for your continued confidence.

Jeff (10/8/2025)

Certain material in this work is proprietary to and copyrighted by iM Global Partner Fund Management, LLC and is used by Bogue Asset Management LLC with permission. Reproduction or distribution of this material is prohibited and all rights are reserved.